Buying your first home is one of the biggest financial decisions you will ever make. Most people step into the process feeling prepared — only to discover that the gaps in their knowledge are more expensive than they expected.

- Why First-Time Buyers Are More Vulnerable to Costly Mistakes

- Skipping Mortgage Pre-Approval Before House Hunting

- Pre-Qualification vs. Pre-Approval — What Actually Matters

- How to Get Pre-Approved Without Hurting Your Credit Score

- Misunderstanding How Much Buying a Home Actually Costs

- Letting the Down Payment Myth Delay the Purchase

- Skipping or Undervaluing the Home Inspection

- What a Standard Home Inspection Does and Does Not Cover

- How to Use Inspection Results Without Losing the Deal

- Choosing the Wrong Mortgage for the Wrong Reasons

- Fixed vs. Adjustable-Rate Mortgages — Matching the Loan to Your Plans

- Why Shopping Multiple Lenders Saves Real Money

- Making Financial Moves That Damage the Loan Application

- What Not to Do Between Pre-Approval and Closing

- How Lenders Verify Your Financial Picture Before Closing

- Ignoring the Neighbourhood When Evaluating the Property

- How to Research a Neighbourhood Before Making an Offer

- Red Flags in a Neighbourhood That Are Easy to Miss

- Moving Too Fast or Too Slow During the Offer Stage

- Not Working With the Right Real Estate Agent

- What to Look for When Choosing a Buyer’s Agent

- Understanding Dual Agency and Why It Can Work Against You

- What These Mistakes Have in Common — and How to Stay Ahead of Them

The good news is that most first-time home buyer mistakes to avoid are completely preventable. They are not the result of carelessness. They happen because nobody hands you a clear guide before you start, and by the time you realise something went wrong, the paperwork is already signed.

This article covers the most common mistakes first-time buyers make at every stage of the process — from pre-approval to closing day — along with straightforward steps to keep each one from derailing your purchase.

Why First-Time Buyers Are More Vulnerable to Costly Mistakes

Buying a home is not like making most other purchases. There is no trial period, no easy return policy, and no clear price tag on the wall. Every step involves professionals who do this every day, while you are doing it for the first time.

That gap in experience puts first-time buyers at a real disadvantage. You may not know what a Loan Estimate document is supposed to look like, what questions to ask during an inspection, or what seller concessions are even possible. When you do not know what you do not know, it is easy to miss things that an experienced buyer would catch immediately.

These are not signs that someone is irresponsible or uninformed. They are the natural result of entering a complex process without a roadmap.

The Emotional Pull of Homeownership

Imagine this: you have been searching for three months. You walk into a house, and it just feels right. The kitchen is exactly what you pictured. The backyard is perfect. You make an offer the same day without running the numbers carefully, and two weeks later, you realise you stretched $40,000 beyond what you should have spent.

That scenario plays out constantly, and it is entirely driven by emotion. Excitement is a normal part of buying a home, but it becomes a liability when it speeds up decisions that should take time. The urgency that comes with a competitive market makes this worse. Buyers start skipping steps not because they want to, but because slowing down feels like it will cost them the house.

The fix is simple to say but harder to practice: set your financial boundaries before you ever visit a property, and treat them as fixed.

How the Buying Process Creates Blind Spots

The home-buying process has many stages, and each one demands attention to different things. Pre-approval focuses on your finances. The property search focuses on location and features. The offer stage shifts to strategy and timing. The inspection is about the condition. Closing involves legal documents.

Most buyers stay sharp during the stages they are most familiar with and lose focus during the ones they do not understand. A buyer who researched loan types thoroughly may not know that their financial behaviour between pre-approval and closing can still affect their loan. Someone who asks the right questions during the inspection may sign a purchase agreement without reading every clause.

No single stage is more important than another. Treating each step with equal attention is the most effective protection against expensive oversights.

Skipping Mortgage Pre-Approval Before House Hunting

One of the most common home-buying errors is starting the property search before getting a pre-approval letter from a lender. It feels logical to look first and figure out financing later. In practice, it creates problems at every step.

Without pre-approval, you do not have a reliable number to work with. You may spend months viewing homes in a price range you cannot qualify for, or make an offer on a property only to find out your financing falls short. Sellers take offers from pre-approved buyers far more seriously, and in competitive markets, many agents will not even show homes to buyers who have not completed this step.

Pre-approval signals to everyone involved that you are a serious buyer with confirmed borrowing capacity.

Pre-Qualification vs. Pre-Approval — What Actually Matters

These two terms are often used as if they mean the same thing. They do not.

Pre-qualification is a basic estimate based on information you self-report: income, debts, and assets. No documents are verified. It takes a few minutes and carries almost no weight with sellers or listing agents.

Pre-approval involves a formal application. The lender checks your credit, reviews pay stubs, bank statements, and tax returns, and issues a conditional commitment based on verified data. That letter tells a seller that a real lender has looked at your financial picture and confirmed you can borrow up to a specific amount.

If you bring a pre-qualification letter to a competitive offer, many sellers will not take it seriously. If you bring a pre-approval letter, you are standing on solid ground.

How to Get Pre-Approved Without Hurting Your Credit Score

Many buyers avoid getting pre-approved early because they worry that multiple lender inquiries will damage their credit score. That concern is understandable, but the system is built to account for rate shopping.

When multiple mortgage lenders pull your credit within a defined window, most credit scoring models count those inquiries as a single hard pull. Depending on the model used, that window is typically between 14 and 45 days. This means you can apply to several lenders, compare Loan Estimates, and choose the best offer without compounding damage to your score.

To get started, gather your last two years of tax returns, recent pay stubs, two to three months of bank statements, and identification documents. Submit applications to at least two or three lenders within the same short window to keep the credit impact minimal.

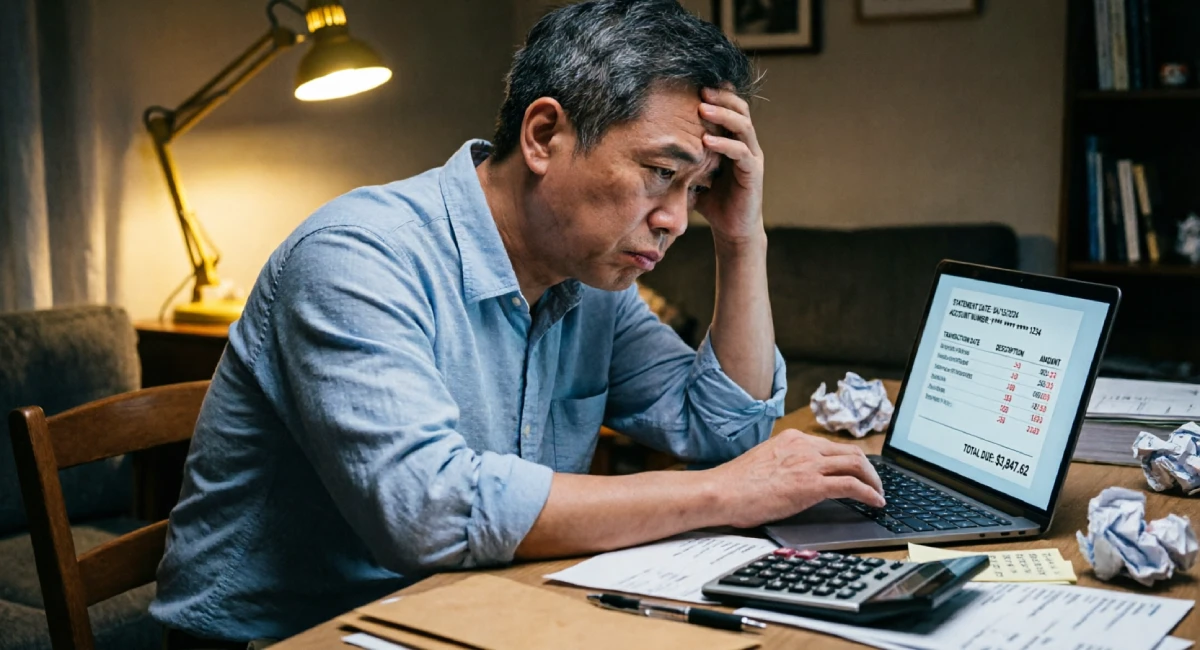

Misunderstanding How Much Buying a Home Actually Costs

A lot of first-time buyers set a budget based entirely on the down payment amount. That is the most visible cost, so it feels like the primary number to focus on. The problem is that it represents only part of what you will actually spend to get the keys in your hand.

The full cost of buying a home includes closing costs, moving expenses, immediate repairs or purchases, and the ongoing costs of ownership. Buyers who account only for the down payment often arrive at closing short on funds or start their homeownership already financially stretched.

Closing Costs That Catch Buyers Off Guard

Closing costs are the fees associated with finalising the purchase and securing the mortgage. They typically range from 2% to 5% of the purchase price and must be paid separately from the down payment.

These costs generally include:

- Lender origination fees

- Title search and title insurance

- Escrow or attorney fees

- Appraisal and inspection fees

- Prepaid property taxes and insurance

- Recording fees

On a $350,000 home, closing costs could range from $7,000 to $17,500. That is real money that needs to be available on closing day. Some buyers are able to negotiate with sellers to cover a portion of closing costs as part of the deal, but this is never guaranteed and should not be counted on during the planning phase.

Ongoing Costs New Owners Rarely Anticipate

The expenses do not stop at closing. Homeownership comes with a set of recurring costs that renters are never responsible for, and first-time buyers often underestimate these significantly.

Regular ongoing costs include:

- Property taxes (vary widely by location)

- Homeowner’s insurance

- HOA fees, where applicable

- Utilities, which tend to be higher than in rental units

- Routine maintenance and unexpected repairs

A practical rule of thumb is to set aside 1% to 2% of your home’s value each year for maintenance and repairs. On a $300,000 home, that is $3,000 to $6,000 annually. Appliances break, roofs age, and plumbing fails. Having that reserve prevents a single repair bill from becoming a financial emergency.

Letting the Down Payment Myth Delay the Purchase

Many first-time buyers believe they cannot buy a home until they have saved 20% of the purchase price. This idea is widespread, and it keeps a significant number of qualified buyers on the sidelines far longer than necessary.

The 20% figure comes from the threshold at which lenders no longer require private mortgage insurance (PMI). It is a real milestone worth reaching if the timing works in your favour. But it is not a requirement to buy a home, and waiting for it can actually cost you more in the long run.

Loan Programs Built for First-Time Buyers

Several loan programs exist specifically to help buyers with smaller down payments qualify for a mortgage:

- FHA loans require as little as 3.5% down for buyers with a credit score of 580 or higher

- Conventional 97 loans allow 3% down and are backed by Fannie Mae and Freddie Mac

- VA loans are available to eligible military service members and veterans with no down payment required

- USDA loans offer zero-down options for buyers purchasing in eligible rural and suburban areas

Each program has its own eligibility criteria, insurance requirements, and loan limits. The trade-off for a lower down payment is typically the cost of mortgage insurance, either built into the rate or paid as a monthly premium. That added cost is real, but it needs to be weighed against the opportunity you might miss by waiting.

When Waiting to Save More Actually Costs More

Here is a scenario worth thinking through carefully. A buyer has $20,000 saved and can afford a home today at $300,000, putting down roughly 6.5% with a conventional loan. They decide to wait two years to save a full 20%, which would be $60,000.

During those two years, home prices in their target area increase 5% per year. The same home now costs approximately $330,750. The 20% down payment is now $66,150. They saved more, but the target moved further away. Meanwhile, they spent two years paying rent instead of building equity.

This will not apply to every market or every situation. But it illustrates why the decision to wait should always be based on current market data rather than an assumption that more time always means a better outcome.

Skipping or Undervaluing the Home Inspection

In a competitive market, buyers sometimes waive the home inspection to make their offer more attractive to sellers. This is one of the most dangerous home-buying errors a first-time buyer can make.

An inspection is not a formality. It is the one opportunity you have to bring an independent professional into the property before the sale is final. Skipping it means you accept the home in whatever condition it is actually in, with no information and no leverage.

What a Standard Home Inspection Does and Does Not Cover

A licensed home inspector evaluates the visible and accessible components of the property. This typically includes the foundation and structure, the roof, HVAC systems, plumbing, electrical systems, windows and doors, and the attic and crawl space where accessible.

What a standard inspection does not cover is equally important. Inspectors do not typically test for:

- Mould or air quality issues

- Pest or termite infestations

- Radon gas

- Underground oil tanks or sewer lines

- Asbestos or lead paint

If any of these are a concern, you will need to hire specialist inspectors separately. In areas with known radon risk, older homes with lead paint concerns, or properties with mature trees near sewer lines, these add-on inspections are often worth the extra cost.

How to Use Inspection Results Without Losing the Deal

An inspection report is a negotiating tool, not a reason to panic or automatically walk away. The key is knowing how to read it.

Every inspection report includes a long list of findings. Most of them are minor: a worn caulk seal around a bathtub, a missing outlet cover, a slow-draining sink. These are maintenance items, not defects. Focus your attention on findings flagged as safety hazards or major system failures.

When significant issues are found, you have several options. You can ask the seller to make specific repairs before closing. You can request a price reduction to cover the cost of fixing the issues yourself. You can ask for a credit at closing. Or you can walk away if the problems are serious enough.

What you want to avoid is requesting a full laundry list of cosmetic fixes in a market where the seller has other interested buyers. Prioritise what actually matters and negotiate strategically.

Choosing the Wrong Mortgage for the Wrong Reasons

The lowest advertised interest rate is not always the best mortgage. This is one of those common buying mistakes that does not reveal itself until years into the loan, when a buyer realises the terms they agreed to were not as favourable as they seemed on the surface.

Choosing a mortgage requires understanding more than the rate. Loan type, repayment term, lender reliability, fee structure, and prepayment penalties all affect the true cost of borrowing.

Fixed vs. Adjustable-Rate Mortgages — Matching the Loan to Your Plans

A fixed-rate mortgage locks in your interest rate for the full life of the loan. Your principal and interest payment stays the same whether you choose a 15-year or 30-year term. This is the right choice for buyers who plan to stay in the home long-term and want payment certainty.

An adjustable-rate mortgage (ARM) starts with a fixed rate for an introductory period, then adjusts periodically based on a market index. A 5/1 ARM, for example, holds the initial rate for five years and adjusts annually after that.

An ARM can make sense for a buyer who is confident they will sell or refinance within the fixed period. The initial rate is usually lower than a comparable fixed rate, which reduces monthly payments during those early years. The risk is that if circumstances change and you stay longer than planned, your payments can increase significantly when the rate adjusts.

Match the loan structure to your actual plans, not to what gives you the lowest payment today.

Why Shopping Multiple Lenders Saves Real Money

On a $300,000 mortgage over 30 years, a difference of 0.25% in interest rate translates to roughly $15,000 to $16,000 in additional total interest paid. That is not a rounding error. It is a real amount that rewards the buyers who take the time to compare.

Get quotes from at least three lenders: a large bank, a regional bank or credit union, and an independent mortgage broker. Compare them using the Loan Estimate, a standardised three-page document every lender is required to provide. Look at the annual percentage rate (APR), not just the interest rate, as the APR includes fees and gives a truer picture of the total cost.

Do all of this within a short window to keep the credit impact minimal.

Making Financial Moves That Damage the Loan Application

Getting pre-approved is a significant step, but it does not mean your financing is secured. The final loan approval happens just before closing, and lenders verify your financial picture again at that stage. Anything that changes between pre-approval and closing day can put the entire deal at risk.

This is an area where buyers make avoidable financial mistakes that fall into the category of avoiding bad deal errors — not because they acted dishonestly, but because they did not know what the rules were.

What Not to Do Between Pre-Approval and Closing

From the moment you receive a pre-approval letter until the day you sign the final closing documents, your financial behaviour needs to stay consistent with what the lender reviewed. Specifically:

- Do not open any new credit accounts, including store cards

- Do not make large purchases, including furniture, appliances, or a new car

- Do not make any undocumented deposits or transfers into your bank accounts

- Do not change jobs unless necessary, and disclose any change to your lender immediately

- Do not pay off large debts in a way that depletes your cash reserves for closing

Each of these actions can change your credit score, your debt-to-income ratio, or your verified cash position. Any of those changes can affect your loan terms or, in serious cases, cause the lender to withdraw approval entirely.

How Lenders Verify Your Financial Picture Before Closing

Most buyers assume that once pre-approval is done, the financial review is complete. It is not.

Lenders typically pull your credit again within a few days of the scheduled closing date. They may also request updated bank statements or a letter of explanation if any new activity appears. A new credit card showing a balance, a significant change in your savings account, or a shift in employment status can all trigger further review.

If your credit score drops before closing due to a new inquiry or a missed payment, your interest rate may increase. If the change is severe enough, the lender may require a revised approval or withdraw the offer completely.

The simplest rule: keep your financial life as stable as possible from the day you apply until the day you close.

Ignoring the Neighbourhood When Evaluating the Property

A house does not exist in isolation. Its value, livability, and long-term appreciation are tied directly to where it sits. One of the most overlooked home-buying errors is spending significant time evaluating the property itself while paying little attention to the surrounding area.

You can improve a home. You cannot move it.

How to Research a Neighbourhood Before Making an Offer

Thorough neighbourhood research does not require expensive tools. Much of what you need is publicly available.

Before making any offer, take the following steps:

- Visit the area at different times of day, including weekday mornings, evenings, and weekends

- Check crime statistics through local government or official police department websites

- Look up the zoning map for the area to understand what can be built nearby

- Review school ratings using official or widely recognised education data sources

- Check local planning commission agendas and meeting minutes for upcoming development projects

- Drive or walk the commute route during actual commute hours, not midday

The goal is to understand what the area looks and feels like in real use, not just on a pleasant Saturday afternoon when the listing photos were taken.

Red Flags in a Neighbourhood That Are Easy to Miss

Some warning signs are subtle enough that even attentive buyers walk right past them.

Watch for:

- Multiple homes are listed for sale on the same street simultaneously

- Nearby businesses are closing or sitting vacant

- Roads, pavements, or public infrastructure in visibly poor condition

- A high concentration of rental properties in a neighbourhood marketed as owner-occupied

- Evidence of deferred maintenance across multiple homes in the same block

- Commercial or industrial zoning immediately adjacent to the residential street

None of these signals is an automatic reason to walk away. But each one warrants a closer look and a direct conversation with your agent about what they might mean for your investment.

Moving Too Fast or Too Slow During the Offer Stage

Timing during the offer stage is one of the less obvious sources of home-buying errors. It works in both directions: moving too fast can lead to overpaying or skipping important due diligence, while moving too slowly in an active market means losing a property you wanted to a buyer who acted with more confidence.

Neither extreme serves you well. The goal is to act with speed when the data supports it and with patience when it does not.

How to Write a Competitive Offer Without Overpaying

Start with the numbers. Your agent should pull comparable sales, known as comps, for similar properties in the same area sold within the last three to six months. This gives you an objective baseline for what the property is actually worth at current market conditions.

From there, you can structure the offer strategically. If the market is highly competitive, an escalation clause can be useful. This automatically increases your offer in defined increments above competing bids, up to a ceiling you set in advance. It keeps you in the running without committing to an inflated price upfront.

Be thoughtful about which contingencies you include. The financing and inspection contingencies exist to protect you. Removing them entirely to win a bidding war is rarely worth the risk.

When to Walk Away From a Deal

Knowing when to stop pursuing a property is just as important as knowing how to compete for one.

Clear reasons to walk away include:

- An inspection reveals significant structural, safety, or system issues that the seller refuses to address or price-adjust for

- The property appraises below the agreed purchase price, and the seller will not renegotiate

- New information surfaces about the neighbourhood or title that was not disclosed earlier

- You have significantly exceeded your original budget to stay competitive, and the financial logic no longer holds

Walking away from a deal is never easy, especially after weeks of searching and negotiating. But a purchase that exceeds your financial limits or carries unresolved problems is not a win. Another property will come along.

Not Working With the Right Real Estate Agent

Many first-time buyers underestimate how much their agent influences the outcome of the purchase. An experienced buyer’s agent who knows the local market, communicates clearly, and understands how to negotiate on your behalf is one of your strongest assets. An inexperienced one, or no agent at all, can leave significant gaps in your protection.

What to Look for When Choosing a Buyer’s Agent

The right agent for you is not necessarily the one with the most listings or the most prominent advertising. For a first-time buyer, the qualities that matter most are:

- Demonstrable experience in the specific local market where you are buying

- A track record of working with first-time buyers and guiding them through the full process

- Clear, responsive communication — you need an agent who keeps you informed at every step

- Full-time availability during your buying window

- Willingness to explain things rather than simply direct you

Interview at least two to three agents before choosing one. Ask directly how many buyers they have represented in the past year, what their approach is to negotiation, and what they would do if an inspection revealed a major problem. Their answers will tell you a great deal about how they will handle your transaction.

Understanding Dual Agency and Why It Can Work Against You

Dual agency occurs when a single agent, or two agents within the same brokerage, represent both the buyer and the seller in the same transaction. It is legal in many markets, but it creates an obvious conflict of interest.

An agent in a dual agency situation cannot fully advocate for either party. They cannot advise the buyer to offer less than the asking price, nor can they encourage the seller to accept a lower offer. They are effectively neutral — which sounds fair, but means you are negotiating without a genuine advocate in your corner.

If you discover that your agent also represents the seller, ask for clarification about what they are and are not able to advise you on. In some cases, the simplest move is to find a buyer’s agent who has no connection to that listing.

What These Mistakes Have in Common — and How to Stay Ahead of Them

Every mistake covered in this article shares the same root cause: entering a complex, high-stakes process without enough preparation. The good news is that preparation is entirely within your control.

The buyers who avoid the most costly first-time home buyer mistakes to avoid are not the ones who happen to be lucky or naturally savvy. They are the ones who did their homework before the search started, stayed patient when emotion tried to take over, and built a team of professionals they could actually trust.

Take the outline of mistakes in this article and treat it as a pre-purchase checklist. Before you make a single offer, make sure you have:

- A verified pre-approval letter from at least two lenders

- A clear and honest budget that accounts for all costs, not just the down payment

- A buyer’s agent who is working exclusively for you

- A plan to keep your financial behaviour stable between pre-approval and closing

- A commitment to inspect every property properly, regardless of how competitive the market feels

The process is long and at times stressful, but every step has a clear logic to it. Work through each one carefully, and the outcome will be a purchase you are genuinely confident in.

If you found this article useful, have a read of the parent guide: What Should First-Time Home Buyers Know Before Starting the Process? — It covers the full picture from the very beginning.